Early Retirement Works Better When the Life You Want Is Easier to Sustain

The Situation

It is easy to picture early retirement as clean math: save enough, invest well, and leave work sooner. That frame is appealing because it turns a deeply human transition into a single target.

But for most households, early retirement is not only about whether the portfolio can support you. It is about whether the life you want can be sustained for a longer period of time. That distinction matters.

The limits of a bigger-number frame

Leaving full-time work earlier shortens the years you have to save and lengthens the years your assets must support spending. It also creates new decisions about Social Security and health coverage.

For people born in 1960 or later, starting Social Security at 62 reduces a $1,000 full‑retirement‑age benefit to about $700 per month. [1]

Retirement also rarely unfolds exactly as planned. In a 2024 national survey, 58% of retirees said they retired earlier than expected, and 31% said their spending was at least a little higher than they could afford. [2] A narrow target can miss the real sources of pressure.

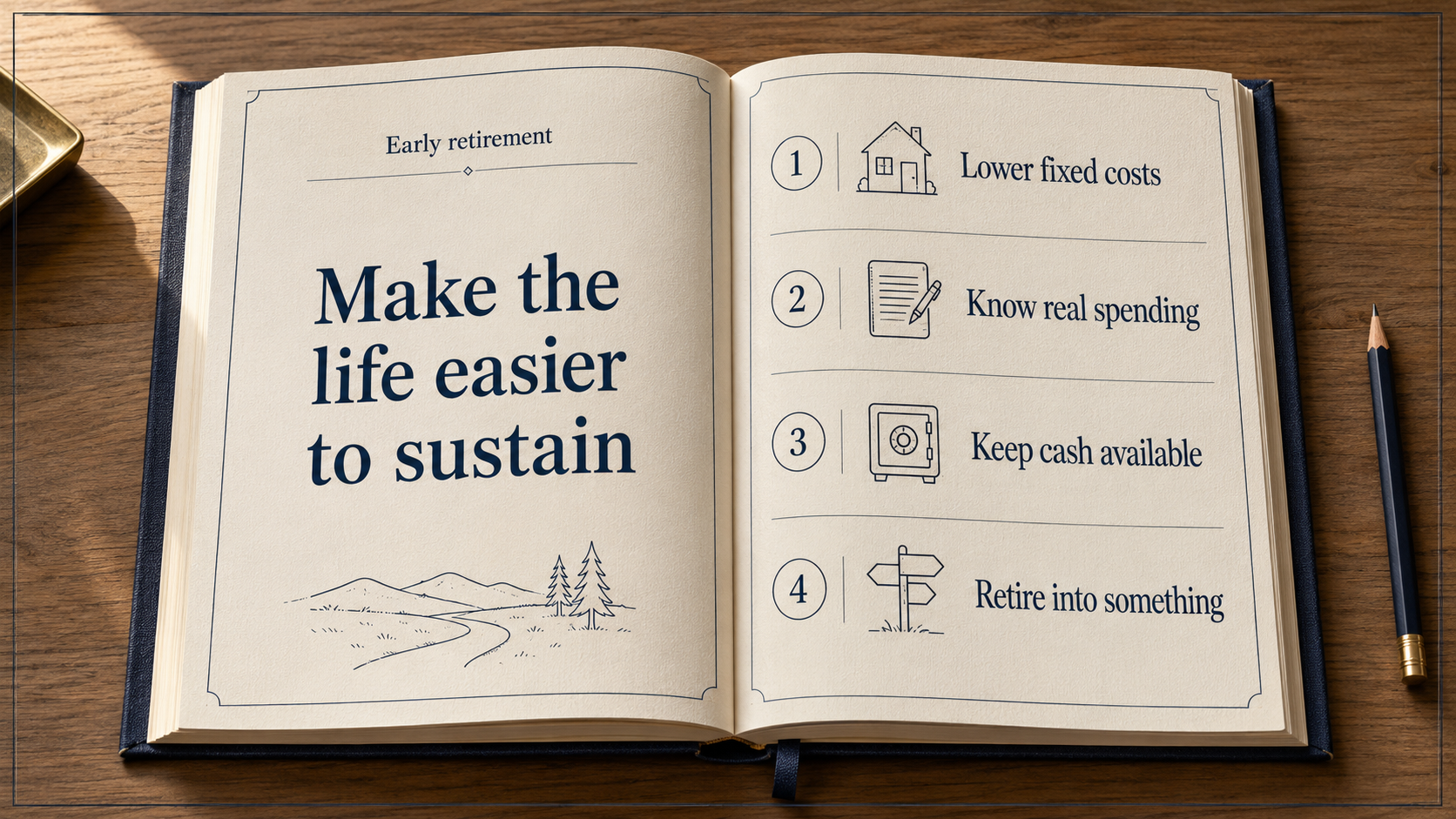

Lower the load your plan must carry

Early retirement works best when you reduce the amount of life your assets have to carry and clarify what retirement will actually cost. That is not deprivation. It is the alignment between what matters and what your plan is meant to support.

This shift moves the question from “Can I afford to quit?” to “What would make this life easier to sustain?” Choices you control, such as fixed costs, flexibility, and how you will spend your time, start to matter most.

Shrink fixed costs without shrinking life

If early retirement is a real priority, today’s lifestyle choices connect directly to tomorrow’s freedom. The more your current life depends on high fixed costs, recurring upgrades, consumer debt, or expensive habits that feel non‑negotiable, the harder it is to step away sooner.

This does not mean life has to become smaller. It means learning the difference between lifestyle and quality of life. One is expensive to maintain. The other is rooted in what actually matters, like time, relationships, energy, contribution, and simplicity.

Define the real cost of retirement

Rules of thumb are a place to start. Early retirement demands more precision. You need a clearer sense of what spending is essential, what spending is optional, and which expenses are temporary or likely to fade over time.

Some costs end when work ends, but others remain and some grow. Fidelity’s 2025 estimate says a 65‑year‑old individual may need about $172,500 in after‑tax savings for health care in retirement.

Retiring before Medicare eligibility often means funding a coverage bridge through the marketplace or other options. [4][5]

Dovetail Principle: Financial Decisions Need to Fit Together.

When lifestyle, claiming age, or coverage timing changes occur, other parts of the plan adjust, which lowers or raises the amount your assets must carry.

Keep enough cash so you can reach

When paychecks stop earlier, resilience matters more. A market decline, home repairs, family needs, or a health surprise can force bad decisions if every dollar of the plan is fully committed.

The Federal Reserve reports that just over half of adults say they have at least three months of expenses set aside. [3]

Early retirement typically calls for more than a symbolic emergency fund. A practical cash buffer can help you avoid selling investments at a loss or pausing important choices under pressure when markets are down. [6]

Retire into something, not just away from work

The fantasy of early retirement often centers on leaving work. The more useful question is what fills the space after work stops being the default structure of the week.

For many people, that answer includes part‑time work, a second business, consulting, teaching, volunteering, or a long‑neglected creative skill. For others, it means family involvement, community, travel, service, or simply a different pace of living.

What this changes when you plan to go early

Once you see early retirement through this lens, the question changes. Instead of asking only whether you can accumulate enough assets fast enough, you start asking whether your life is becoming easier to sustain.

Are you lowering fixed costs? Are you clear about future spending? Are you building enough cash flexibility? Are you stepping toward a version of retirement that has rhythm and purpose, not just free time? Connecting the math to real life is usually where early retirement succeeds or fails.

About the author

Ross Marino, CFP®, CeFT®, is the Founder & CEO of Dovetail Financial and creator of Human-First Financial Guidance®. He helps people nearing or living in retirement connect their lives and wealth so that financial decisions become clearer, more personal, and easier to navigate.

Notes

- Social Security Administration, “Born in 1960 or later: Your full retirement age is 67,” SSA Benefits Planner. Accessed May 2026. Social Security Administration

- Employee Benefit Research Institute, “2024 Spending in Retirement Survey,” Nov. 7, 2024. ebri.org

- Board of Governors of the Federal Reserve System, “Report on the Economic Well‑Being of U.S. Households in 2024 — Savings and Investments,” May 2025. federalreserve.gov

- Fidelity Viewpoints, “How to plan for rising health care costs,” Mar. 13, 2026 (reflecting the 2025 Fidelity Retiree Health Care Cost Estimate: $172,500 for an individual age 65). fidelity.com

- KFF, “Medicare and the Marketplace — FAQs,” Accessed May 2026. kff.org

- Morningstar, “Sequence of Returns: What It Means and How to Deal,” Accessed May 2026. morningstar.com

Disclosure: This content is provided by Dovetail Financial Group LLC (“Dovetail Financial”) for informational and educational purposes only. It is not intended as, and should not be construed as, individualized investment, tax, legal, or accounting advice; a recommendation to buy or sell any security; or a recommendation to adopt any investment strategy. Because each person’s situation is unique, readers should consult their own financial, tax, and legal professionals before taking action based on this content.

Information contained herein is believed to be reliable, but its accuracy or completeness is not guaranteed. Any opinions expressed are current as of the date of publication and are subject to change without notice. All investing involves risk, including the possible loss of principal. Asset allocation and diversification do not guarantee profits or protect against losses in declining markets. Past performance is not a guarantee of future results. Dovetail Financial Group LLC is a registered investment adviser. Registration does not imply a certain level of skill or training. Additional information about Dovetail Financial Group LLC, including Form ADV Part 2A and Form CRS, is available at adviserinfo.sec.gov. © 2026 Dovetail Financial Group LLC. All rights reserved.