A steadier way to think about market highs and lows

A steadier way to think about market highs and lows

New highs and sharp pullbacks both grab attention. They also tempt investors to act on the moment’s feeling. The better question is not “What is the market doing?” but “What changes for us if we react right now?”

A steadier frame starts with how your plan carries market changes. That means seeing time horizons, cash needs, risk levels, and review triggers before deciding whether anything should change.

Why headlines can pull you off course

Highs can make risk feel smaller than it is. Lows can make long-term goals feel further away than they are. Either way, the emotional signal is strong while the decision context is often incomplete.

Market timing promises control in uncertainty. In practice, it requires two correct calls, when to get out and when to get back in, and it is difficult to do consistently.

Reader-facing sources describe market timing as a prediction-led strategy and show that staying invested often wins over time. [2][5][4]

What your plan should show before you react

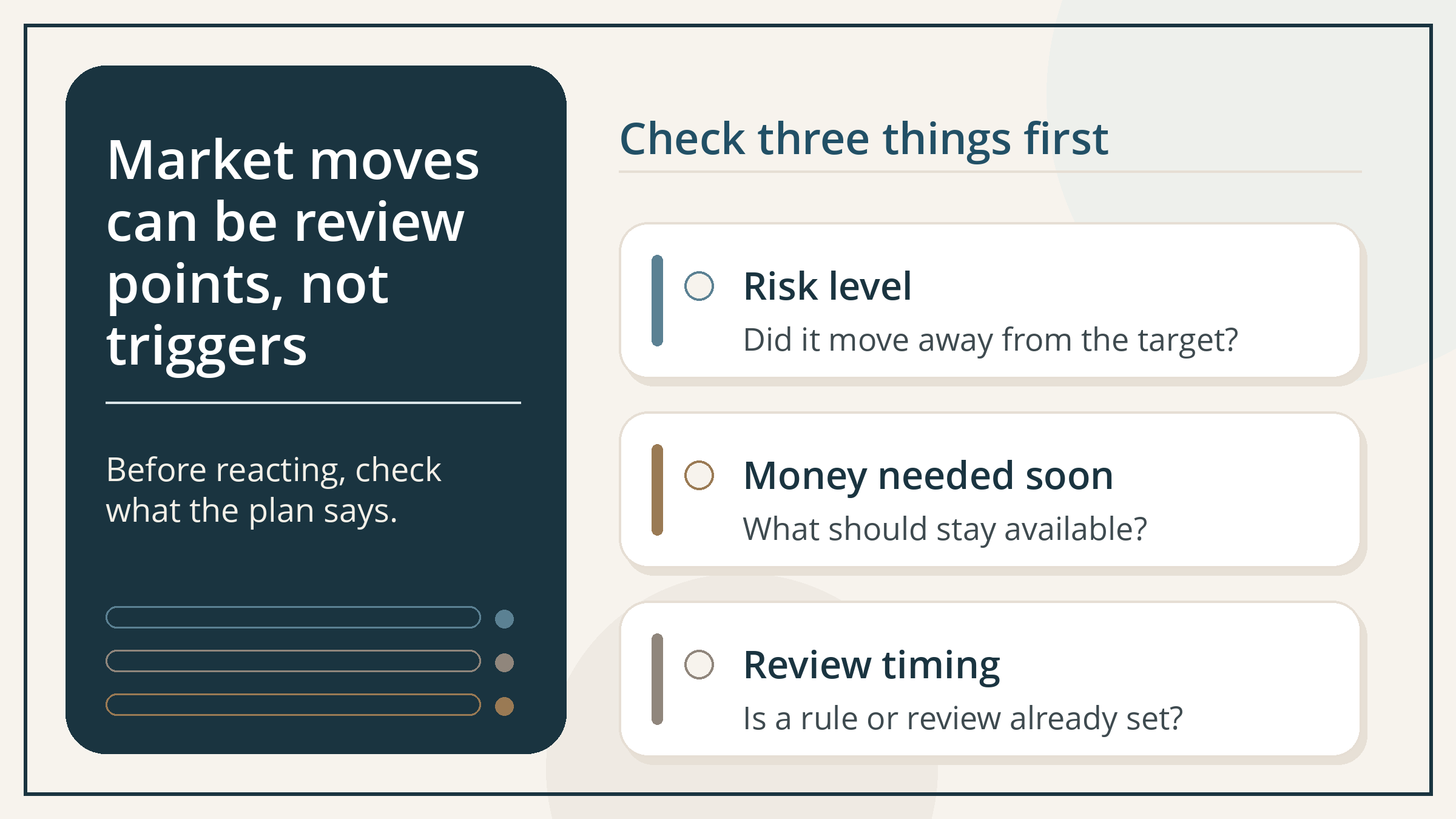

Before you change investments on a headline, check the three basics. First, your time-horizon map. What money supports the next one to three years, three to seven years, and later?

Second, your cash and withdrawal needs. What must stay available, and when? Third, your risk level now versus the target. Did gains push you beyond your intended risk, or did declines push you below it?

Dovetail Principle: Planning helps you decide when the future is unclear.

A clear structure shows what can be decided now and what can be reviewed as conditions change.

Keep risk in line with disciplined rebalancing

Rebalancing trims what ran ahead and adds to what lagged. It helps keep your chosen risk mix intact without having to guess the next move. Done on a schedule or at set thresholds, it reinforces “buy lower, sell higher.” [1]

When markets run up, rebalancing can reduce the chance that a future drop hurts more than intended. When markets fall, rebalancing can refill underweight growth assets inside your targeted range rather than trying to pick a turning point. [1][5]

Why “find the right manager” is not the whole answer

If reacting means hunting for someone to time your moves for you, keep perspective. SPIVA’s latest U.S. Scorecard reports that 79% of active large-cap funds underperformed the S&P 500 in 2025, and long-horizon underperformance rates remain high.

That makes consistent outperformance hard to rely on as a decision plan. [3]

A plan-led process does not deny the existence of skill. It treats headlines and results as inputs to your review cadence rather than signals to overhaul the portfolio.

For retirees, highs and lows feel different

If you are withdrawing from your portfolio, a bad stretch early in retirement can put more pressure on future income than the same returns in a different order. A plan may pair a modest cash or short-term reserve with an investment mix that supports growth for later years. [6]

The goal is not to predict swings. It is to reduce the need to sell long-term assets at low prices to fund near-term spending. [6]

Turn market moves into review points, not reactions

Use a simple filter when headlines hit: - Does our risk mix now differ meaningfully from the target? Rebalance if ranges are breached. [1] - Did anything in our time horizon or cash needs change?

- Is there a rule-based review already on the calendar? Let the plan’s cadence, not the news cycle, set most changes.

This approach does not ignore markets. It makes them legible. Highs and lows become inputs to a plan you can carry, not triggers you must chase.

About the Author

Ross Marino, CFP®, CeFT®, is the Founder & CEO of Dovetail Financial and creator of Human-First Financial Guidance®. He helps people nearing or living in retirement connect their lives and wealth so that financial decisions become clearer, more personal, and easier to navigate.

Notes

- SEC Investor.gov , “Beginners’ Guide to Asset Allocation, Diversification, and Rebalancing,” accessed May 15, 2026. investor.gov

- SEC Investor.gov , “Risk and return,” accessed May 15, 2026. investor.gov

- FINRA , “What Is Market Timing?,” 2025, accessed May 15, 2026. FINRA

- S&P Dow Jones Indices, “SPIVA U.S. Year‑End 2025,” March 3, 2026. spglobal.com

- Dimensional Fund Advisors, “We Found 30 Timing Strategies that ‘Worked’—and 690 that Didn’t,” October 2023, accessed May 15, 2026. dimensional.com

- Morningstar, “Staying Invested Beats Timing the Market—Here’s the Proof,” 2023, accessed May 15, 2026. morningstar.com

- Vanguard, “Retirement risks and how to manage them,” accessed May 15, 2026. investor.vanguard.com

Disclosure: This content is provided by Dovetail Financial Group LLC (“Dovetail Financial”) for informational and educational purposes only. It is not intended as, and should not be construed as, individualized investment, tax, legal, or accounting advice; a recommendation to buy or sell any security; or a recommendation to adopt any investment strategy. Because each person’s situation is unique, readers should consult their own financial, tax, and legal professionals before taking action based on this content.

Information contained herein is believed to be reliable, but its accuracy or completeness is not guaranteed. Any opinions expressed are current as of the date of publication and are subject to change without notice. All investing involves risk, including the possible loss of principal. Asset allocation and diversification do not guarantee profits or protect against losses in declining markets. Past performance is not a guarantee of future results. Dovetail Financial Group LLC is a registered investment adviser. Registration does not imply a certain level of skill or training. Additional information about Dovetail Financial Group LLC, including Form ADV Part 2A and Form CRS, is available at adviserinfo.sec.gov. © 2026 Dovetail Financial Group LLC. All rights reserved.