The Tax Move That Changes More Than Taxes

The Situation

If retirement is getting close, it is natural to look at states with no income tax and wonder whether a move would let you keep more of what you have built. The attraction is real.

In 2026, several states levy no individual income tax, and some other states do not tax IRA and 401(k) distributions, even though they still tax other income.[1][2]

Why a lower-tax state can be tempting

Lower recurring taxes can matter. If a meaningful share of your retirement paycheck will come from IRA withdrawals, pension income, taxable investment income, or business proceeds, state tax rules can affect what you actually keep.

States do not all tax retirement income the same way. Depending on where you live, Social Security benefits, retirement account distributions, capital gains, property taxes, and sales taxes may be treated differently.[2][3]

Why taxes alone can mislead

State income tax is only one layer of the picture. Sales, property, and estate taxes can offset part of the apparent advantage. In 2026, only a handful of states have no statewide sales tax, while states such as Tennessee and Washington sit near the top on combined state and local sales taxes.

Property taxes vary just as widely.[4]

Some well-known no-income-tax states, including Texas and New Hampshire, are also on the higher end of the property-tax spectrum, while states such as Nevada and Wyoming are much lower.[2][5]

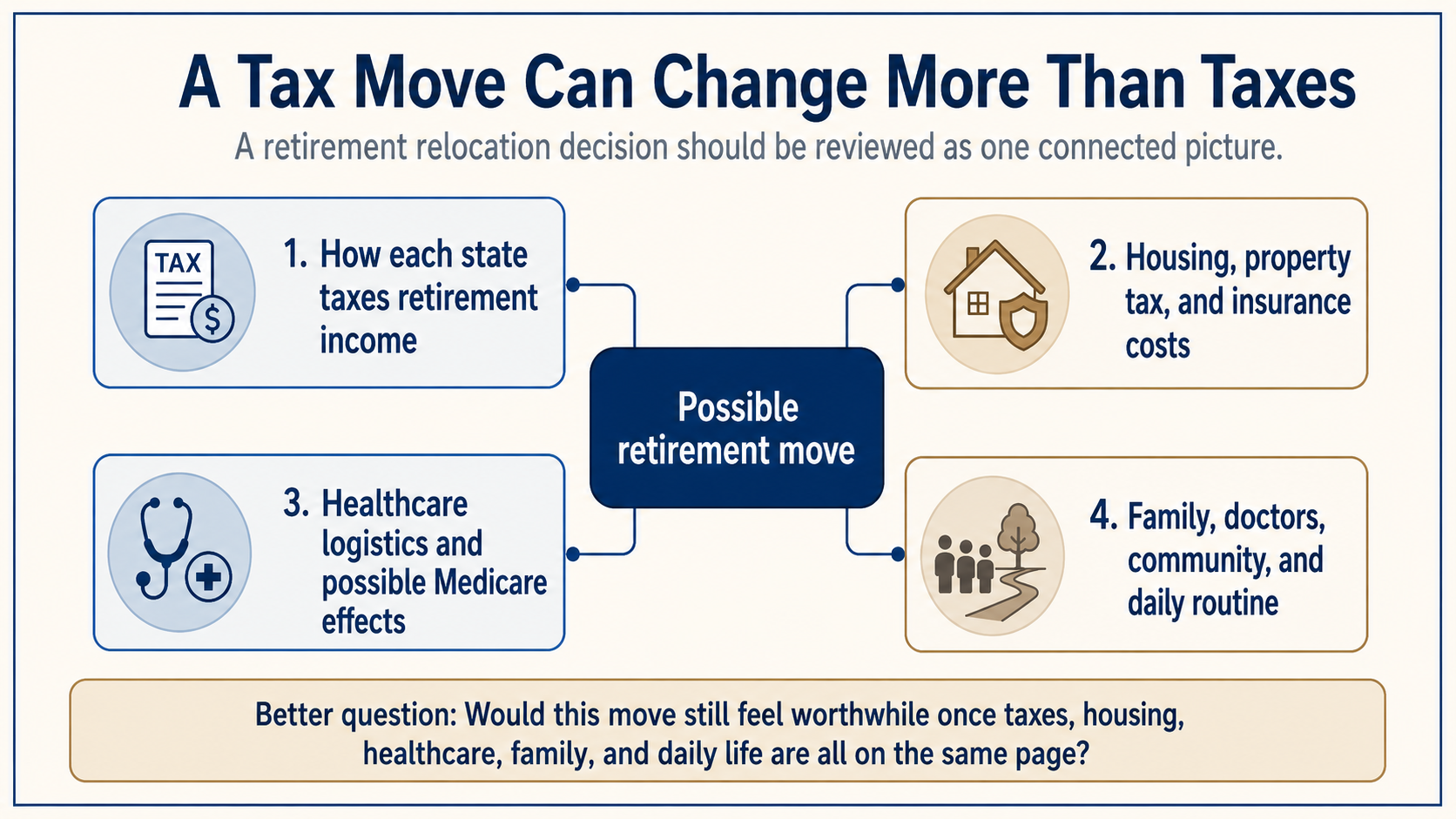

Dovetail Principle: Financial Decisions Need to Fit Together.

A relocation decision affects multiple taxes and living costs at once, so the decision should be evaluated as a single, interconnected picture.

Not all “tax-friendly” states are friendly in the same way

New Hampshire is a good example. It has no state income tax and no statewide sales tax, but its effective property tax rate was about 1.50 percent in 2024, the fifth-highest in the country.[5] Tennessee shows the opposite mix.

Its property taxes are relatively low, but its average combined state and local sales tax rate is about 9.61 percent, the second-highest in the nation.[4] Texas is another reminder that no income tax does not automatically mean low overall taxes, with an average combined sales tax rate near 8.20 percent and an effective property tax rate around 1.40 percent.[4][5]

Florida remains broadly favorable for many retirees, with no state income tax, middle-of-the-pack combined sales taxes, and moderate property taxes. Washington shows the point from a different angle: it has no broad-based income tax, but it does tax certain long-term capital gains and also imposes an estate tax.[2][3]

What each side of the decision is trying to protect

One side of the crossroads is trying to protect efficiency. If you can reduce recurring taxes in a meaningful way, you may create more room for spending, gifting, travel, or simply breathing easier about cash flow.

The other side is trying to protect continuity. Staying put can preserve proximity to family, established doctors, community ties, and routines, and foster the feeling that retirement is built on a familiar foundation rather than a major reset.

How to structure the decision

A better relocation decision usually begins with structure, not with a map. Start by listing the income sources that are most likely to fund retirement in the first five to ten years. Then compare how each state would treat those sources.[2][3]

After that, layer in the rest of the cost picture: property taxes, sales taxes, housing costs, insurance, and healthcare logistics.

Then look at the one-time economics of the move. Selling a main home may qualify for a federal gain exclusion of up to $250,000 for a single filer or $500,000 for a married couple filing jointly, but not every household will fit cleanly inside that result.[4][5][6]

A higher-income year can have spillover effects beyond the tax return itself. Medicare Part B and Part D premiums rise at higher income levels, so a large gain or other income spike can matter in more than one place.[7]

The better retirement question

The better question is not, “Which state is cheapest for retirees?” It is, “Would this move materially improve our after-tax life once taxes, housing, healthcare, family, and continuity are all on the same page?”

Sometimes the answer will be yes. Sometimes the better answer will be to stay where you are and optimize within the state you already know. The goal is not to chase the lowest tax line in isolation. It is to make a retirement decision that supports both the balance sheet and the life it serves.

About the Author

Ross Marino, CFP®, CeFT®, is the Founder & CEO of Dovetail Financial and creator of Human-First Financial Guidance®. He helps people nearing or living in retirement connect their lives and wealth so that financial decisions become clearer, more personal, and easier to navigate.

Notes

- Tax Foundation, “State Individual Income Tax Rates and Brackets, 2026,” February 17, 2026. taxfoundation.org

- AARP, “13 States That Don’t Tax IRA and 401(k) Distributions,” updated March 18, 2026. aarp.org

- AARP, “State Tax Guides: What You’ll Owe in the 2026 Tax Season,” updated March 18, 2026. aarp.org

- Tax Foundation, “State and Local Sales Tax Rates, 2026,” January 20, 2026. taxfoundation.org

- Tax Foundation, “Property Taxes by State and County, 2026,” March 16, 2026. taxfoundation.org

- Internal Revenue Service, “Topic No. 701, Sale of Your Home,” last reviewed January 22, 2026; and Internal Revenue Service, “Publication 523 (2025), Selling Your Home,” last reviewed March 3, 2026. IRS and IRS

- Centers for Medicare & Medicaid Services, “2026 Medicare Parts A & B Premiums and Deductibles,” November 14, 2025. CMS

Disclosure: This content is provided by Dovetail Financial Group LLC (“Dovetail Financial”) for informational and educational purposes only. It is not intended as, and should not be construed as, individualized investment, tax, legal, or accounting advice; a recommendation to buy or sell any security; or a recommendation to adopt any investment strategy. Because each person’s situation is unique, readers should consult their own financial, tax, and legal professionals before taking action based on this content.

Information contained herein is believed to be reliable, but its accuracy or completeness is not guaranteed. Any opinions expressed are current as of the date of publication and are subject to change without notice. All investing involves risk, including the possible loss of principal. Asset allocation and diversification do not guarantee profits or protect against losses in declining markets. Past performance is not a guarantee of future results. Dovetail Financial Group LLC is a registered investment adviser. Registration does not imply a certain level of skill or training. Additional information about Dovetail Financial Group LLC, including Form ADV Part 2A and Form CRS, is available at adviserinfo.sec.gov. © 2026 Dovetail Financial Group LLC. All rights reserved.