Succession Is Not One Decision: How the Pieces Fit Together Near Retirement

The Situation

For many business owners, succession is framed as a future event. One day, you will decide when to step back, who will take over, and how the handoff will work. Near retirement, it rarely feels that simple.

The business may provide income, represent a large share of net worth, carry a family legacy, and support employees simultaneously. No wonder succession feels heavy. It is a cluster of connected choices, not a single yes-or-no.

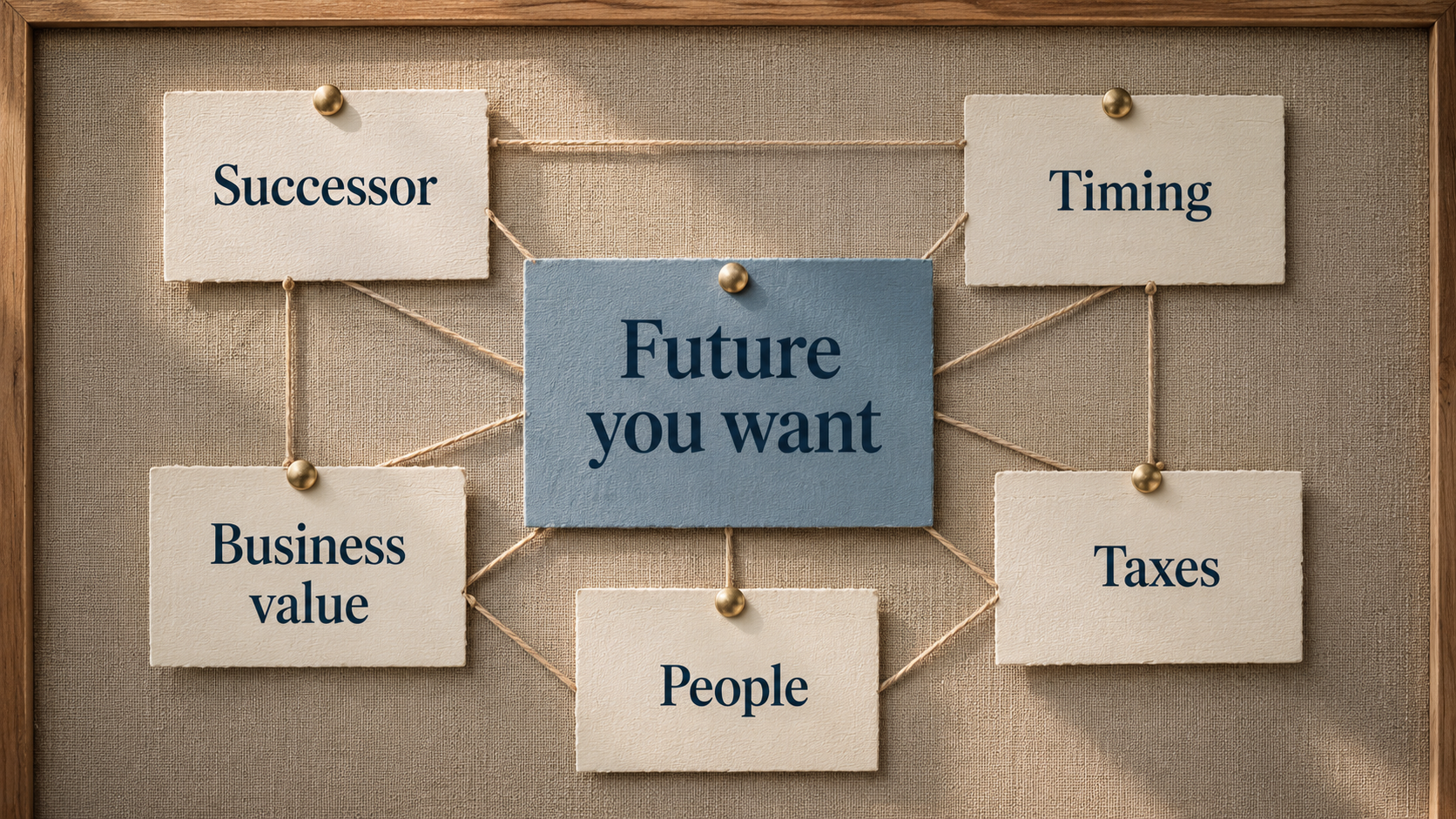

Start with the future you want

Clarity improves when you begin with the future you want, then choose the mechanics that support it. The successor you prefer can affect your timeline. Your timeline can affect valuation. Valuation shapes retirement cash flow expectations, deal structure, and taxes.

Structure then influences what family members receive, how employees experience the change, and how much control you retain. A clearer plan does not erase tradeoffs. It helps you see them earlier, while you still have time to decide.

Successor choice changes more than leadership

Choosing a successor can look like a people decision. It is also financial and strategic. A family member, an internal buyer, a management team, or an outside buyer brings different financing realities, timelines, governance approaches, and communication needs.

There is no single model that fits every family business. In practice, effective transitions weigh leadership requirements against ownership and governance choices, and they often compare internal and external candidates before selecting a path. [1]

Timing and valuation move together

Many owners think about valuation only when they are close to a sale. Often, that is too late. Time creates options. It can allow leadership development, cleaner financials, operational improvements, and a more deliberate transfer structure.

When a sale or transfer is likely, independent valuation work by qualified appraisers helps anchor expectations and deal design. Professional standards exist for business valuation, and planning earlier gives you room to act on what the valuation reveals.

Practical succession guides also emphasize building the plan before urgency forces choices. [2][3]

Dovetail Principle: Financial Decisions Need to Fit Together.

Seeing how successor, timing, valuation, taxes, and people decisions interact helps you choose a path that protects what matters most.

Taxes follow structure, not just price

The sale price alone does not tell you the outcome. For a business sale, federal rules generally treat the deal as the sale of separate assets, and buyers and sellers must allocate the price across those assets using the residual method.

That allocation affects the gain or loss on each asset and the buyer’s basis going forward. [4]

Family transfers add another layer. If you sell or transfer an interest to family for less than full value, gift tax rules may apply to the difference between the value and the amount received.

That does not make every family transfer the same. It does mean legal, tax, and estate pieces belong in the conversation from the beginning, not as late paperwork. [5]

People and communication carry the plan

A plan can look complete on paper and still struggle in practice if expectations are unclear. Employees wonder what will change. Family members infer different promises. Key partners look for stability. Successors need authority that matches responsibility.

Recent global family business research highlights that governance, communication, and clarity of purpose remain central issues for family firms, not side topics. Aligning ownership, leadership, and communication with the chosen path increases the odds that the transition will work in practice. [6]

A clearer landscape makes the next step easier

Succession reaches beyond ownership. It touches retirement income, taxes, family fairness, leadership continuity, legacy, and identity. That is why it deserves a broader lens.

Instead of asking only, 'Who will take over,' it is often more useful to ask, 'How do these decisions affect each other, and what future are we trying to create?' When the landscape becomes clearer, the next step usually does too.

Not because every tradeoff disappears, but because you can finally see which decisions belong together and which ones should come first.

About the author

Ross Marino, CFP®, CeFT®, is the Founder & CEO of Dovetail Financial and creator of Human-First Financial Guidance®. He helps people nearing or living in retirement connect their lives and wealth so that financial decisions become clearer, more personal, and easier to navigate.

Notes

- Harvard Business Review, “Plan a Smooth Succession for Your Family Business,” September 13, 2022. hbr.org

- American Society of Appraisers, “ASA Business Valuation Standards,” accessed May 15, 2026. appraisers.org

- U.S. Chamber of Commerce, “7 Steps to Creating a Succession Plan that Keeps Your Business on Track,” March 22, 2024. uschamber.com

- Internal Revenue Service, “Sale of a Business,” Page Last Reviewed or Updated February 10, 2026. IRS

- Internal Revenue Service, “Instructions for Form 709 (2025), United States Gift (and Generation-Skipping Transfer) Tax Return,” accessed May 15, 2026. IRS

- PwC, “PwC’s 12th Family Business Survey: Reclaiming advantage,” 2025, accessed May 15, 2026. pwc.com

Disclosure: This content is provided by Dovetail Financial Group LLC (“Dovetail Financial”) for informational and educational purposes only. It is not intended as, and should not be construed as, individualized investment, tax, legal, or accounting advice; a recommendation to buy or sell any security; or a recommendation to adopt any investment strategy. Because each person’s situation is unique, readers should consult their own financial, tax, and legal professionals before taking action based on this content.

Information contained herein is believed to be reliable, but its accuracy or completeness is not guaranteed. Any opinions expressed are current as of the date of publication and are subject to change without notice. All investing involves risk, including the possible loss of principal. Asset allocation and diversification do not guarantee profits or protect against losses in declining markets. Past performance is not a guarantee of future results. Dovetail Financial Group LLC is a registered investment adviser. Registration does not imply a certain level of skill or training. Additional information about Dovetail Financial Group LLC, including Form ADV Part 2A and Form CRS, is available at adviserinfo.sec.gov. © 2026 Dovetail Financial Group LLC. All rights reserved.