Before You Give, Name the Question

The Situation

Americans gave an estimated $592.5 billion to charity in 2024. That headline reminds us that generosity is alive and well. For people making larger or more intentional gifts, the harder part is knowing what question to ask before the money leaves the account. [1]

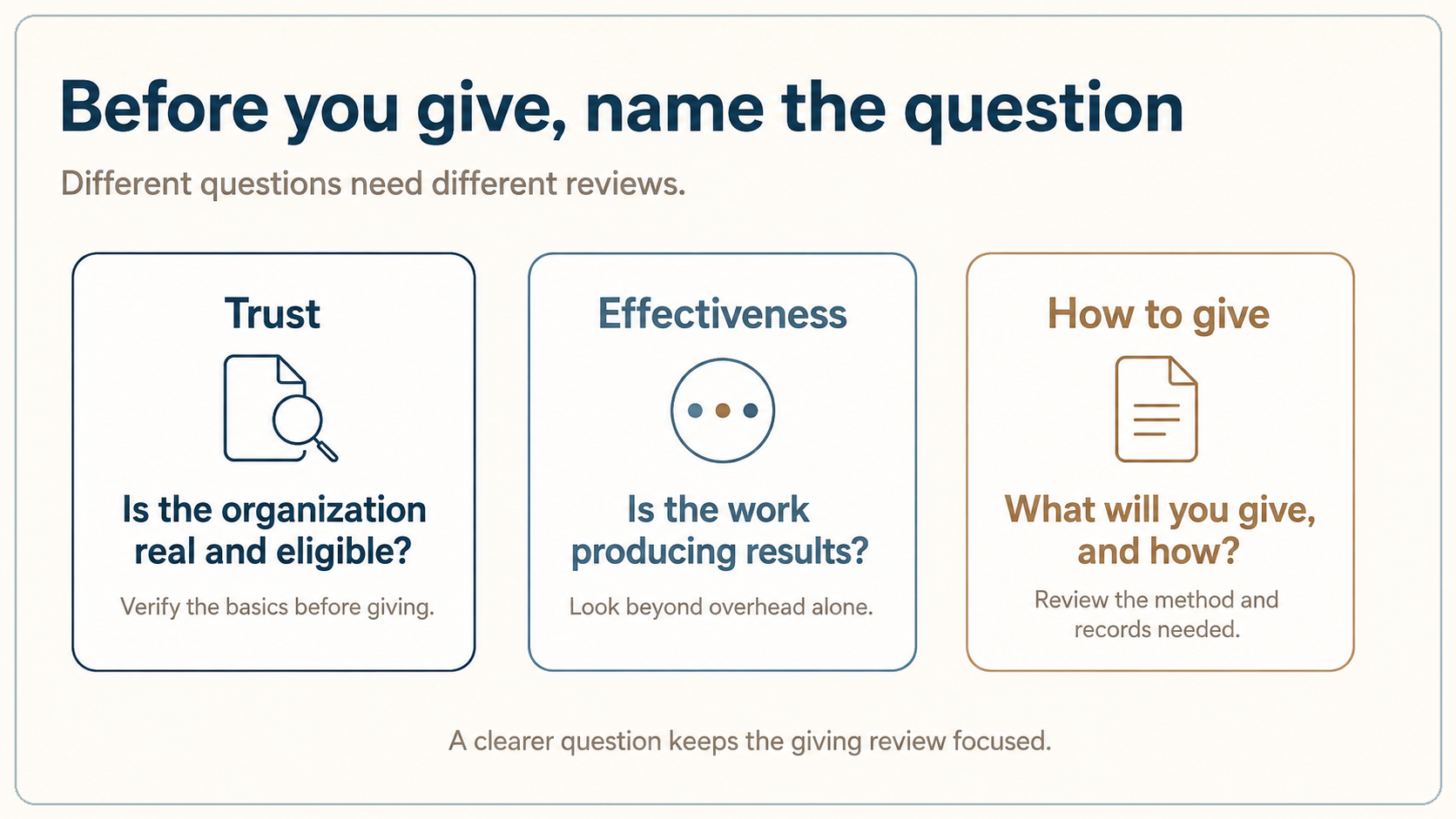

When people say, “I want to make sure this charity is worth supporting,” they often treat it as one decision. In practice, they may be asking about trust, effectiveness, or how the gift should be made.

Naming which one you are actually asking keeps your review focused and manageable.

Why the first question matters

Before you donate, listen to which statement sounds most like you. Are you unsure whether the organization is real, current, or eligible for tax-deductible gifts? Do you believe it is legitimate, but you are not sure it uses resources well?

Or do you trust the charity, but wonder whether cash is the right way to give?

Your answer reveals the problem you are solving and points to a clearer next step. This sorting step helps prevent two common mistakes. One is chasing impact metrics while basic eligibility remains unverified. The other is stopping at a comfortingly low overhead ratio when the better question is whether the work produces results.

Dovetail Principle: Planning helps you decide when the future is unclear.

Before the gift is made, the first step in planning is to name the question. Are you verifying the organization, judging its effectiveness, or deciding how the gift should be made? Each question points to a different kind of review.

If the problem is trust and legitimacy

If your uncertainty starts with basic credibility, begin with verification. The IRS Tax Exempt Organization Search (TEOS) lets donors confirm whether an organization is eligible to receive tax-deductible contributions. It also lets donors review public filings and determination letters.

Churches and some governmental units may not appear, but TEOS remains the primary public check. [2]

Independent information services can help you gather public data in one place. Candid’s tools surface profiles, financials, and leadership details, which makes a quick legitimacy scan easier.

If you cannot confirm deductible status, cannot find recent filings or leadership information, or only see vague program descriptions, treat those as reasons to slow down before giving. [3]

If the question is effectiveness, not legitimacy

Once a charity passes the legitimacy test, the question changes: is the work being done thoughtfully and effectively? This is where many donors fall into the overhead trap, the mistaken belief that program-versus-overhead ratios alone reveal nonprofit quality.

Sector leaders have urged donors to look beyond raw expense splits to evidence of outcomes, learning, and improvement. [4]

Modern rating frameworks reflect that shift. Charity Navigator’s methodology evaluates areas such as Impact & Measurement and Accountability & Finance, not just expense ratios. Low overhead can signal efficiency, or it can signal underinvestment in the people and systems that make results possible.

Interpret costs in context and look for evidence that the charity measures results and learns from what it finds. [5][6]

When the issue is how to give

Sometimes the charity is credible and the mission fit is clear.

The remaining issue is how the gift is made: what will you give, and what account or method will you use? IRS rules treat charitable gifts differently depending on the asset, the type of recipient, and your records. That is why appreciated securities may be worth reviewing before defaulting to cash.

Documentation rules also matter. [7]

A donor-advised fund (DAF) can separate the timing of the tax deduction from the timing of grants. You contribute assets, take an immediate deduction if you itemize, and recommend grants to public charities over time.

That does not make a DAF automatically better. It may fit situations where timing or multi-year grants are part of the problem you are solving. It can also fit gifts of assets that take more coordination. [8]

Volunteering, receipts, and paper trails

Not every contribution has to be cash. Skills-based volunteering can be a meaningful form of support. From a tax perspective, you generally cannot deduct the value of your time or services. Certain unreimbursed out-of-pocket expenses related to that work may qualify. [7]

One practical step should never be skipped: documentation. For any single contribution of $250 or more, a contemporaneous written acknowledgment from the charity is generally required. A generous gift without a clean paper trail can become an avoidable tax problem. [7]

Give with a clearer question

The common mistake in charitable giving is not always choosing the wrong charity. Often, it is misidentifying the question. If the real issue is trust, verify. If the real issue is effectiveness, look beyond overhead to outcomes.

If the real issue is how the gift is set up, decide what to give and how to give it. That is a better standard for thoughtful giving. Not just, “Do I like this cause?” but, “What kind of giving decision am I actually making?”

About the author

Ross Marino, CFP®, CeFT®, is the Founder & CEO of Dovetail Financial and creator of Human-First Financial Guidance®. He helps people nearing or living in retirement connect their lives and wealth so that financial decisions become clearer, more personal, and easier to navigate.

Notes

- Giving USA 2025: U.S. charitable giving grew to $592.50 billion in 2024, lifted by stock market gains, Giving USA, June 24, 2025, accessed May 15, 2026.

- Search for tax-exempt organizations (TEOS), Internal Revenue Service, last reviewed May 6, 2026, accessed May 15, 2026.

- Research nonprofits, funders, and grants, Candid, accessed May 15, 2026.

- Changing the nonprofit narrative: Debunking the overhead myth (again), Candid, March 17, 2026, accessed May 15, 2026.

- Impact & Measurement methodology, Charity Navigator, accessed May 15, 2026.

- Accountability & Finance methodology, Charity Navigator, accessed May 15, 2026.

- Publication 526, Charitable Contributions and Charitable organizations: substantiation and disclosure requirements, Internal Revenue Service, accessed May 15, 2026.

- What is a Donor-Advised Fund?, National Philanthropic Trust, accessed May 15, 2026.

Disclosure: This content is provided by Dovetail Financial Group LLC (“Dovetail Financial”) for informational and educational purposes only. It is not intended as, and should not be construed as, individualized investment, tax, legal, or accounting advice; a recommendation to buy or sell any security; or a recommendation to adopt any investment strategy. Because each person’s situation is unique, readers should consult their own financial, tax, and legal professionals before taking action based on this content.

Information contained herein is believed to be reliable, but its accuracy or completeness is not guaranteed. Any opinions expressed are current as of the date of publication and are subject to change without notice. All investing involves risk, including the possible loss of principal. Asset allocation and diversification do not guarantee profits or protect against losses in declining markets. Past performance is not a guarantee of future results. Dovetail Financial Group LLC is a registered investment adviser. Registration does not imply a certain level of skill or training. Additional information about Dovetail Financial Group LLC, including Form ADV Part 2A and Form CRS, is available at adviserinfo.sec.gov. © 2026 Dovetail Financial Group LLC. All rights reserved.